Showing posts with label real estate. Show all posts

Showing posts with label real estate. Show all posts

Rent by Price Ratio: Real Estate Valuation by Rent

Continuing our RealT valuation

series, we now bring to you – Rent by Price ratio. In our post – “Valuation by Rental Prospects - Real Estate

Valuations” we discussed how an individual should take into

consideration the rental prospects while valuing a property. Today let’s

discuss whether or not a prospective rent enough?

Facing dilemma: Which property to select?

Many a times, we get confused

making choices between different assets. It becomes tough to select one from a

choice of 2-3 properties. In such confusions, the decision is generally made

based on only apparent features (aesthetics, size, location, ease of

transaction etc.). To provide a rationale to this dilemma, we bring to you the

concept of Rent by Price ratio (RP ratio).

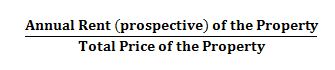

Rent by Price Ratio (RP)

As is self-explanatory from its

name, RP ratio means:

This gives you a fraction which

can be used very effectively for evaluating more than one property together. To

state in simple words, this ratio gives you the percentage of initial price

that you can recover per annum by rental income.

How to make the choice?

Let’s take a scenario that you

have a choice to make from among the following options:

|

Property

|

Prospective

Rent

|

Price

|

RP

Ratio

|

|

Prop1

|

INR 25,000 pm

|

INR 7.5 million

|

4.00%

|

|

Prop2

|

INR 20,000 pm

|

INR 5.5 million

|

4.36%

|

Source:

Real Scenario of 2 properties in Hyderabad, India

As both the properties provide

awesome investment opportunities and are located opposite to each other, it

becomes increasingly difficult to make a choice among the 2.

But looking at the last column

(RP ratio) in the above table, it becomes very clear that Prop2 provides a

return of 4.36% against 4.00% of Prop1.

Hence it makes more sense to go

for Prop2, than for Prop1.

Dilemma Solved, Decision Simplified B-)

Closing Thoughts: We formulated the above concept and analysis

while facing a dilemma on making the choice on the above 2 properties only.

This RP ratio provided us a yardstick to go for Prop2 & we followed it; you

may not. It’s just indicative, not a sure shot approach to making decision.

------ Thanks for reading RealT

Horizon J ------

G+2: An Emerging Real Estate Model

As we said in our earlier post that we went to the fields in Jaipur to explore this sector further, today we

share with our readers a prevalent model in this space. During our visit to

actual sites and meeting with various people closely associated with RealT, we

came across a model that is highly prevalent in Tier 2 cities at present. Let’s

share some insights on this topic.

What exactly is G+2?

Due to recent developments, Tier

2 cities have stringent land by-laws. These laws restrict unplanned and uneven

growth of these cities which are on their way to become mega cities. One such

by-law restricts the vertical growth of town to a certain limit, based on the

size of plot and width of the road on which the plot is located.

|

| A typical G+2 construction |

Paying full respect the laws,

Builders & Developers have devised an alternative to make optimum use of

the available plot and have come up with the concept of Ground+2 floors. Now depending on the designs prepared by the

Architect, Builder can erect 4-6 flats on that small piece of land. Generally these

plans are designed in a way that there is ample space for parking of 4-6

vehicles alongside the building. If the dimensions of plot doesn’t allow ample

parking space, Builder can even go for Stealth floor for parking. Even in this

case, the next 3 floors will be counted as G+2.

|

| G+2 with stealth floor |

Benefits of G+2

- Ideal for mini-builders

- Cost of construction minimizes due to economies of scale (multiple constructions on the same piece of land)

- Pretty good profit margin

- Easy to sell

- Time-to-complete the project is small

Why is it lucrative for mini-builders?

Small Investors and new entrants

prefer this model of RealT so much so that you would see hundreds of such

projects going on in Jaipur all around. The reason being:

Low cost of Entry

|

These projects can be initiated with relatively small amount of money

as compared to traditional huge projects.

|

Minimized Risk

|

Even if all the flats are not booked, the builder is safe as he is

sitting on a valuable asset.

|

Funding Operational Costs

|

The operational costs of next floor can be funded by the bookings of

previous floor.

|

Controlled Expansion

|

The builder is free to pull back from going deep into the project at any

time.

|

Closing Remarks: Want to foray into Real Estate? – Go for the

above model, but don’t forget to do a proper market analysis for demand side!

---- Thanks for reading. Your comments will help

us improve our analysis. J ----

Financing - Funding a Real Estate Project

We got a feedback from some of

our readers that our last post Ownership

- Holding a RealT was a bit too

much complicated to understand for a beginner. Totally respecting their valuable

comments, we have tried to mellow down this post on RealT Financing (although

the topic is way more complicated than the last one :-/).

The whole idea of Mortgage Broking is depicted in the above figure. Few points about this process:

What is Financing?

So coming back to the main business, the second level of Value

Chain in Real Estate circumference – Financing. Just as you

require money to pay for your household items, you need money to pay for your

house (realty property) too. But financing a RealT deal is not as simple as

buying vegetables down the street! More often than not, realty buyers need a

proper plan, strategy and an agency to finance their dream projects. This is

where this post originates J

How is Financing classified?

There are several ways in which a RealT deal can be financed. Typically

all the ways can be classified under 2 heads – Equity & Debt.

To start with, we will cover the Debt portion in this post and try to

explain the various options to raise finance through debt.

Debt

Debt, in literal sense means – “raising money from the market for a

particular time horizon, at some interest rate”. Due to the advancement in the

financial markets, many instruments have been developed to carry out this

function. These instruments, if used rationally can benefit both lenders &

borrowers, but improper use of such instruments can even lead to catastrophes

like ‘Sub-prime crisis of 2008’.

Bank Loans

Raising money from a commercial bank is the

easiest way for an individual investor. Banks offer attractive interest rates

to the borrowers and are easily accessible. But this may not be the most

effective way to finance a real estate deal due to the following reasons:

- Banks disburse loans for short-term

- The amount of disbursement depends on various factors like – individual’s net worth, MPBF (maximum permissible bank fund), income statements, securitization etc.

- Indian Banks generally do not grant loans to a new real estate developer

- Banks generally do not grant loans on ‘land’ alone

Mortgages

Mortgage typically means taking loan from a

party by pledging your property as a collateral against the loan. The mortgagee

reserves full right to take a control over the pledged property in case of

foreclosure (default, in simple terms).

Whatever you will read after this point is a

bit complicated, but we have tried to simplify the concept as much as possible.

Let’s see how much sense it makes. So, mortgages can be carried out in 2 ways:

Mortgage Broker:

The whole idea of Mortgage Broking is depicted in the above figure. Few points about this process:

- Brokers are independent agencies, having tie-ups with fund providers

- Fund providers generally prefer these brokers so that the borrower is already researched for credit worthiness

- Mortgage brokers are generally not involved in ‘loan servicing’

- They don’t use their own capital to fund the borrowers

Mortgage Banker:

These are specialized agencies which provides

mortgages directly to the borrowers, using their own capital. These agencies do

not accept deposits from the public, rather makes money from the loan

origination fees & servicing fees.

They typically packages the loans & sell

them to the institutional buyers or government sponsored enterprises in secondary

markets. In US, there are Freddie Mac & Fannie Mae to carry out these

functions while in India there is no such institution yet for this function.

The nearest equivalent that can be thought of is Mortgage

Risk Guarantee Fund.

We know that this has become a bit too much

complicated to understand, but the following diagram may relieve our brain

nerves a bit ;-)

So the whole process of Secondary

Markets is depicted in the above figure. It shows step by step process followed

by the loans to finally reach the borrower.

Note: We understand that this post has been a bit too much complicated.

Please feel free to write to us in case you need any explanations on any of the

above topics. The remaining portion of financing by equity will be covered in

our next post. Stay tuned!!

----- Keep Reading RealT Horizon J

-----

Understanding the reality in RealT – Generic Real Estate Value Chain

As soon as I sat down to pen the

first post for RealT Horizon, I was

bombarded with several areas of concern which need to be addressed here. To start

with, I decided to go with the basics. So let’s look at the overview of the

Value Chain of this sector.

Real Estate Value Chain typically comprises of 5 broad levels:

Figure 1: Broad levels of Real

Estate Value Chain

These 5 steps more-or-less comprise

all the possible activities that one can associate with the development and transaction

of a property. Of course some of the blocks shown above do interchange their positions

sometimes, depending on the usage category. I will try to touch on that aspect

later, or in the following posts. But before that, the usage categories:

Whether the 5 levels shown in

figure 1 will remain intact or some of them will get merged or eliminated

depends totally on the 3 usage categories. If, for instance, the category is ‘Residential’ and that too for single

housing, probably the ‘Transactions’

level can be skipped.

Let me dig a little deeper in the

value chain. If expanded, the chain will take the following shape:

Figure 2: Detailed Generic Real

Estate Value Chain

As can be seen in the above

figure, each level can be further fragmented into several components. This is

the multiplicity that results in all the complexities that this sector is

facing currently in India and probably in various other developing nations.

This sector needs treatment, and

it will be possible only if there is a subtle understanding of its basics ingrained in all the investors. I will cover all the components individually in my future

posts. So stay tuned and pour in your comments & suggestions to help me

analyze RealT Sector more effectively!

Forward detailed links to each level:

Forward detailed links to each level:

- Ownership - Holding a RealT

- Financing - Funding a RealT

- Financing the RealT by Equity

- Construction of a RealT Project

- Transacting & Using your RealT

- - - - - Thanks for reading J - - - - -